Picture this: a chaiwala in Mumbai turns his roadside stall into a mini-chain with a ₹10 lakh Mudra loan. Happened last year. Now, in 2026, schemes like that are easier than ever to grab online.

Small businesses fuel India's economy—think 63 million MSMEs employing 120 million people, per the Ministry of MSME's 2025 dashboard. But cash flow? That's the killer. Good news: 2026 brings beefed-up loan programs with zero-collateral options and digital apps that cut the red tape.

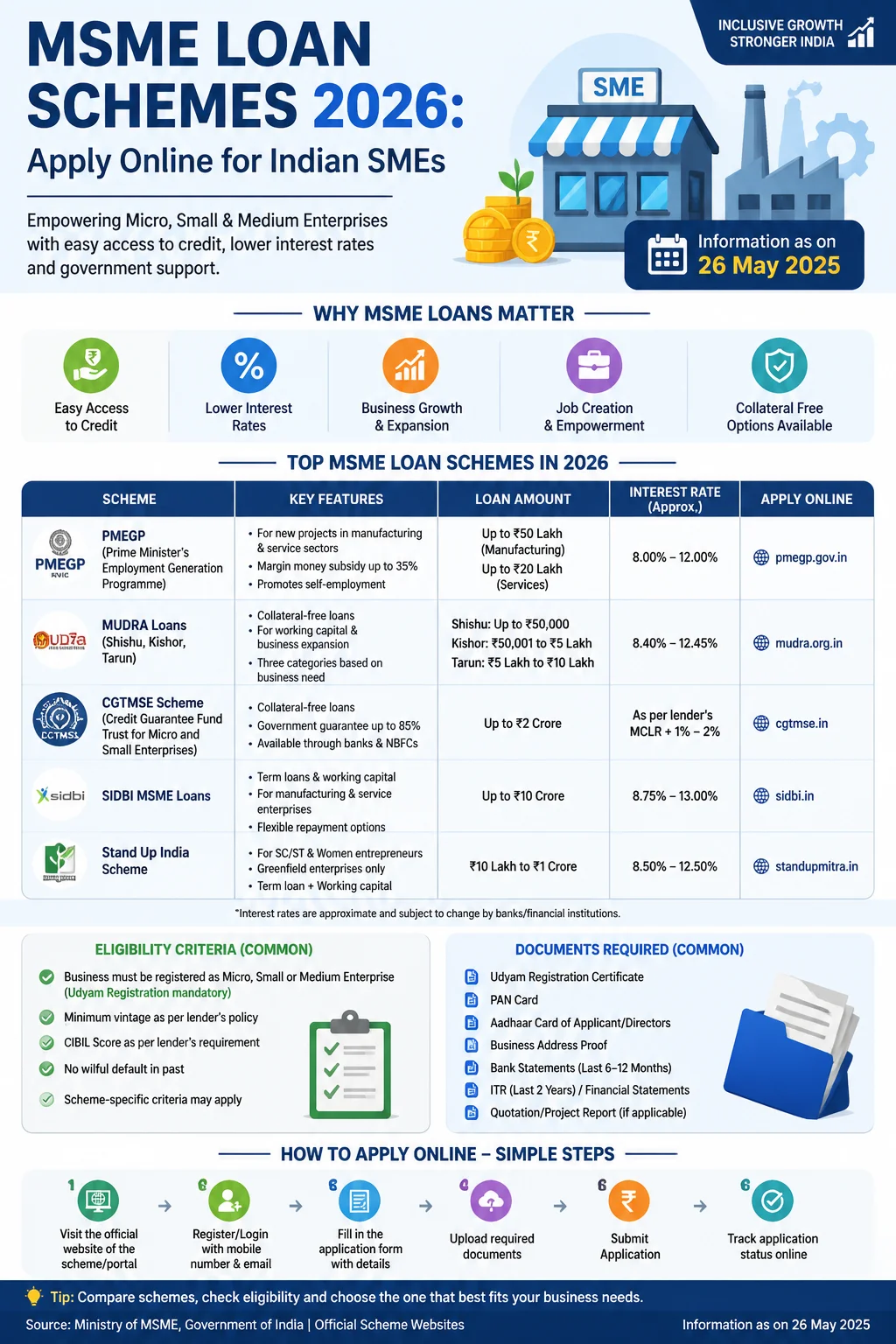

Key MSME Loan Schemes for 2026

Pradhan Mantri Mudra Yojana (PMMY) leads the pack. It's collateral-free up to ₹20 lakh now, with Shishu (₹50k), Kishore (₹5 lakh), and Tarun categories. Disbursements hit ₹45 lakh crore by March 2026, says RBI's latest bulletin—up 15% from 2025.

Then there's CGTMSE, the Credit Guarantee Fund. Banks lend up to ₹5 crore without collateral, and the government guarantees 75-85% of it. Perfect for manufacturers hit by supply snags.

Don't sleep on Stand-Up India either. Targets SC/ST and women entrepreneurs with ₹10 lakh to ₹1 crore loans. Finance Minister Nirmala Sitharaman doubled its fund to ₹20,000 crore in Budget 2026 announcements.

New Twist: Digital MSME Credit Portal

Launched in late 2025, the Udyam Assist portal ties everything together. One login for PSB Loans in 59 Minutes, SIDBI's SMILE, and even NBFC options. I've seen tailors in Surat approve ₹2 lakh in under 48 hours through it.

Who Qualifies? Straight Talk

First, register on Udyam portal—free, Aadhaar-based, takes 10 minutes. MSMEs are micro (turnover <₹5 cr), small (<₹50 cr), medium (<₹250 cr). But here's the catch: 80% of rejects stem from incomplete Udyam profiles, per a 2025 IFC study on Indian SMEs.

Your biz needs 6+ months operation for most schemes. Credit score above 700 helps—check it free on CIBIL's site. Women-led? Extra points under 2026 tweaks.

Step-by-Step: Applying Online

- Log into Udyam portal or PSB's 59minutes site. Use Aadhaar OTP.

- Pick scheme—say PMMY. Fill basics: PAN, GSTIN, turnover proof (ITR/Form 26AS).

- Upload docs digitally. AI scans them instantly—no branch visits.

- Bank assigns a relationship manager. E-approval in 1-7 days if score's solid.

- Funds hit account via NEFT. Track status on GeM portal for govt buyers.

Pro tip: Apply via SBI, HDFC, or Canara first—they process 60% of MSME loans, RBI data shows.

Docs You'll Need (No Excuses)

- Aadhaar, PAN, bank passbook (last 6 months).

- UDYAM certificate—your golden ticket.

- GST returns (GSTR-3B for 2 quarters), ITR (2 years).

- Project report: Simple 2-pager on how you'll use the cash. Templates on SIDBI site.

- Photos of your setup. Makes it real.

Honesty pays. Fudge numbers? CIBIL blacklist for 7 years. Seen it tank a Delhi bakery's dreams.

Tips That Actually Work

Build credit early—pay vendor bills on time via Razorpay or PhonePe. Boosts score 50 points fast.

But wait. Interest rates hover 8-12%—cheaper than informal lenders at 24%. Still, compare: Axis offers 9.25% for women under Stand-Up.

Anyone who's bootstrapped knows: pair loans with free MSME tools like Zoho Books for bookkeeping. Cuts default risk by 30%, per KPMG's 2025 SME report.

Plot twist. Rejections? Appeal via bank's grievance portal or RBI's Sachet app. 40% overturns in 2026 so far.

Real Stories, Real Wins

Take Priya Sharma, owner of a Jaipur handicraft unit. Grabbed ₹15 lakh via CGTMSE in Feb 2026. Exports doubled to US buyers. Or Raju in Coimbatore—₹8 lakh Mudra loan bought CNC machines. Output up 200%.

These aren't outliers. Ministry data: 12 million loans sanctioned digitally in FY26 Q1 alone.

So, what's stopping you? Dust off that Udyam cert. Click apply. Your stall could be the next chain. Just do the paperwork right—regret's the real loan shark.